Guest Post: The Wealth Stylist, Natasha M. Campbell, Success and Money Coach

Sticking to a budget is one of the biggest money challenges many Americans face. According to a 2013 Gallup poll, only one in three American households prepare a detailed, monthly written, or computerized, budget that tracks their income and expenses. That means 2 out of 3 households say, “No, thank you” to having a plan for their money.

For many, the “B” word (budget) signals deprivation. If you’ve ever been on a diet, you tend to crave what you shouldn’t have because it’s a form of restriction. The same feeling can be true with your money. Instead of looking at ways you can cut things out of your life, a spending plan focuses on meeting your financial goals and values.

Here are five simple steps to create a spending plan to give your dollars some direction.

What is Your “Why”?

Identify what you want to accomplish. Why does it matter? When you look back a year from now, how will you know that your efforts have been successful? Envisioning your “why” will motivate you to take action. Keep a money journal to remind yourself of your goals and recognize your progress.

Where Are You Now?

To get a hold of your finances, it is important to know where you stand. Review your spending to see if it’s in line with your priorities. Consider printing the last three months of your bank statements and list everything you spent during that timeframe. A 90-day financial view will provide a better understanding of your money. You may forget transactions that only happen on a quarterly basis, like getting the oil changed on your car or receiving bonuses from work.

Image via CreateHer Stock

Identify What’s Not Working

Take inventory of what’s not working in your financial life that is moving you away from your goals. What is holding you hostage from improving your finances? Do you spend out of control when you’re emotional? Simple reflective questions will help you become aware of what’s stopping you from creating a healthy relationship with your money.

Choose a Customized Plan

There is more than one way to create a spending plan, so choosing the right one is important. The 50/30/20 rule is personally one of my favorites. This rule breaks down spending habits into three categories with percentages. Based on your income, essential expenses (like utilities, food, and rent) make up 50% of your spending. Unnecessary expenses (cable, the internet, cell phone) make up 30% of the budget, and future goals (debt payments, savings, retirement fund) make up the remaining 20%.

In the event of a major life experience, a bare bones budget is ideal. A bare bones budget is based on your lowest possible monthly income. If you’re self-employed, work on a commission-based job, or find yourself in financial distress due to job loss or a medical condition, this type of plan will work best for you. Create a plan based on absolute necessities, such as food, shelter, clothing, and transportation.

Image via CreateHer Stock

Track Your Progress

Stay connected to your plan. If you deviate from your spending plan, breathe and forgive yourself. Remain committed to the process. Review your spending plan and make healthy adjustments as needed. Every month is different, so update your spending plan accordingly for special occasions.

Natasha M. Campbell, the Wealth Stylist, is an entrepreneur, wife, mother, personal finance coach, and certified educator. You can find her @wealthstylist just about everywhere!

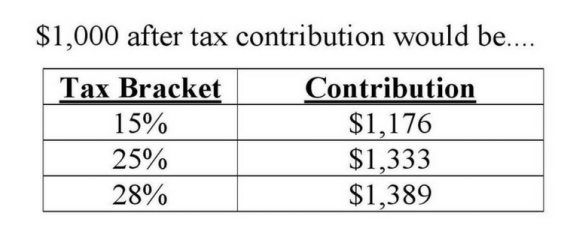

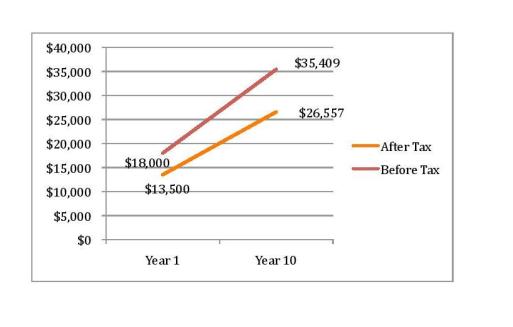

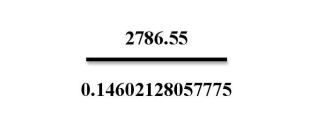

If the retiree’s tax bracket is the same as it was during her working years, it’s a wash between Roth contributions and pre-tax contributions. But if the retiree is in a lower tax bracket in retirement, which is usually the case, deferring taxes provides more money for retirement.

If the retiree’s tax bracket is the same as it was during her working years, it’s a wash between Roth contributions and pre-tax contributions. But if the retiree is in a lower tax bracket in retirement, which is usually the case, deferring taxes provides more money for retirement.

West Virginia University College of Law Graduation May 12, 2012

West Virginia University College of Law Graduation May 12, 2012